Vol 6 No 1 (2026)

Vol 6 No 1 (2026)

Published: 2026-01-13

Research Article

Pages 55-77

Noor Zulfiqar, Muhammad Tayyab Shafi, Kinza Ali, Muhammad Usman Asif, Satyadhar Joshi, Sana Kazi

Noor Zulfiqar, Muhammad Tayyab Shafi, Kinza Ali, Muhammad Usman Asif, Satyadhar Joshi, Sana Kazi

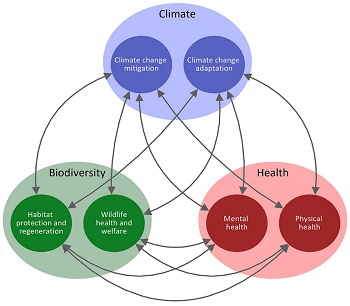

This study examines the complex interactions and trade-offs among energy development, biodiversity conservation, and human livelihoods within the context of increasing global energy demand and sustainability challenges. Using a mixed-methods approach that integrates literature review, case study analysis, and primary empirical data (n = 120), the study provides both quantitative and qualitative insights into stakeholder perceptions and socio-ecological impacts. Quantitative results indicate that environmental degradation (mean = 4.28) and livelihood disruption (mean = 4.05) are perceived as major consequences of energy development, with statistically significant differences across stakeholder groups (p < 0.05). Correlation analysis further reveals a strong relationship between environmental degradation and livelihood insecurity (r = 0.57, p < 0.01). Qualitative findings reinforce these results, highlighting concerns related to habitat loss, unequal benefit distribution, and limited community participation. The findings demonstrate that trade-offs are highly context-specific and vary across energy types and governance settings. Fossil fuel-based energy systems are associated with greater long-term ecological degradation and pollution, whereas renewable energy projects, although comparatively less harmful, still generate localized impacts such as land-use change and habitat fragmentation. These outcomes are particularly significant in biodiversity-sensitive and resource-dependent regions, where livelihoods are closely linked to ecosystem services. To advance current research, this study introduces an Energy--Biodiversity--Livelihood Trade-off Framework, which integrates energy performance, biodiversity integrity, and livelihood outcomes into a unified analytical model. In addition, a region-specific Energy--Biodiversity--Livelihood Trade-off Index (EBL-TI) is proposed to quantify socio-ecological trade-offs across different contexts. The study further operationalizes the Kunming--Montreal Global Biodiversity Framework for the energy sector by linking global targets to measurable governance and planning indicators. Overall, the results highlight the need for integrated and adaptive governance approaches that incorporate biodiversity-sensitive spatial planning, equitable benefit-sharing mechanisms, and inclusive stakeholder participation. By combining empirical evidence with conceptual innovation, this study contributes to advancing sustainable energy transitions that are not only efficient but also ecologically responsible and socially equitable.

Pages 29-54

Philipp Ivanovich Vysikaylo

Purpose: This study applies Vysikaylo's paradigm of cumulative-dissipative systems (CDS), originally developed in physics, to the analysis of socio-economic and political processes in states. CDS theory describes open systems in which convective cumulation and dissipation of energy--mass--momentum fluxes (EMMF) occur. The purpose of this research is to reinterpret classical political economy through the CDS framework by modeling the processes of accumulation, transformation, and dissipation of human and economic potential in states using approaches derived from natural statistical sciences.

Methods: Political and economic phenomena--including the cumulation, transformation, and dissipation of capital and social resources--are modeled using mathematical analogies with physical CDS systems. The study introduces androgenic and gynogenic configurators to represent structural mechanisms in economic systems. Two generalized principles are applied: (1) Lomonosov's conservation law (later experimentally confirmed by Lavoisier), and (2) Clausius's Virial Theorem, according to which only part of the potential energy entering a partially open system remains within it while the rest dissipates into the surrounding environment. Dynamic Order Parameters (PDO) are proposed to quantify systemic dynamics in states viewed as living social CDS systems.

Results: The analysis suggests that similar mechanisms of co-organization observed in physical CDS systems also occur in socio-economic structures, including the circulation of capital, resources, and human potential. When the systemic balance between accumulation and dissipation is disrupted, structural crises, institutional instability, or state transformation may occur. The proposed PDO framework enables quantitative assessment of systemic stability and provides analytical tools for evaluating policies aimed at sustaining state development.

Conclusion: Adjustments in the distribution of national production between elites and the broader population, together with economic policy instruments such as customs duties and industrial protection measures, may contribute to the stabilization and revitalization of weakening states. The CDS-based framework also allows demographic and migration dynamics to be analytically evaluated. Case analyses of Russia, Spain, France, Germany, and the United States illustrate the applicability of the proposed approach. The integration of CDS theory with socio-economic analysis offers a potential foundation for further development of a systematic "science of law" governing social CDS systems.

Pages 18-28

Muhammad Tayyab Shafi, Noor Zulfiqar, Fawad Inam

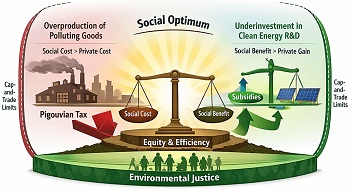

This article explores the critical role of externalities both positive and negative in shaping environmental market dynamics and influencing resource allocation. Positive externalities such as clean energy innovation and public education often lead to underinvestment in beneficial activities due to unaccounted societal gains. Conversely, negative externalities like industrial pollution, deforestation, and overfishing result in market overproduction, imposing environmental and health costs on society. The article assesses various government interventions subsidies, public provision, patent systems, regulations, Pigouvian taxes, and market-based instruments like cap-and-trade to correct these market failures. Drawing on empirical evidence and theoretical frameworks, it evaluates the effectiveness of such policies in promoting sustainability, innovation, and equitable outcomes. Ultimately, the study emphasizes the necessity of well-designed and targeted government action to internalize external costs and benefits, enabling efficient, equitable, and environmentally sustainable market operations.

Pages 1-17

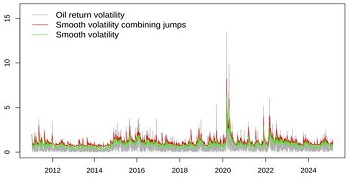

Global Oil Price Jumps and China’s New Energy Sector: New Evidence from Dynamic Volatility Models

Chuanguo Zhang, Yujie Du

Intensifying geopolitical tensions have recently amplified fluctuations in global crude oil prices, where abrupt price jumps often transmit complex spillovers across energy markets. This paper investigates the asymmetric, heterogeneous, and lagged impacts of oil price jump shocks on China's new energy industry at both aggregate and sub-industry levels spanning the full upstream-midstream-downstream industrial chain. Using an ARMA-EGARCH-ARJI framework, global oil price dynamics are modeled to capture volatility clustering and discrete jumps, while expected/unexpected and lag structures are applied to examine asymmetric and delayed responses. The results reveal a unique asymmetric pattern of dual inhibition/promotion: both expected increases and decreases in oil prices suppress new energy returns, whereas unexpected jumps stimulate the sector. The effects are heterogeneous across sub-industries, with upstream sectors showing weaker sensitivity to anticipated shocks. Moreover, the influence of oil price jumps unfolds with notable time lags. These findings underscore the evolving interplay between market-oriented energy transformation and policy stability, offering implications to enhance the resilience and efficiency of China's new energy transition.